In News:

- According to a recent report - Scars of the pandemic - published by the Reserve Bank of India (RBI), the Indian economy is expected to overcome losses arising out of the pandemic (that hit the country in March 2020) only by 2034-35.

- It is RBI’s first detailed analysis of the impact of the pandemic, included in its annual publication on currency and finance.

What’s in today’s article: Highlights of the Report

Highlights of the Report:

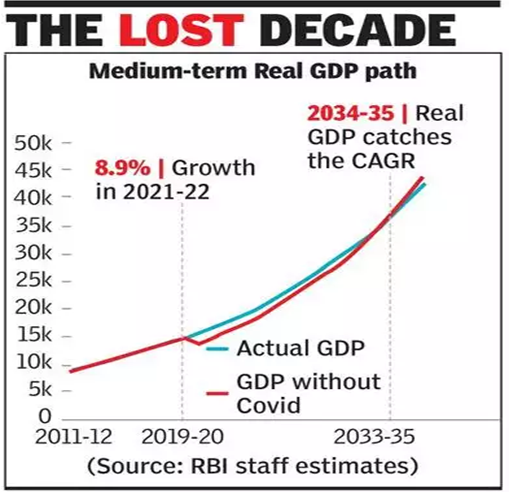

- Output losses during pandemic: The output losses for individual years have been calculated to be Rs 19.1 lakh crore, Rs 17.1 lakh crore and Rs 16.4 lakh crore for 2020-21, 2021-22, and 2022-23, respectively (adding up to Rs 52.6 lakh crore).

- Reasons for the loss:

- Stringency of the lockdown as the most cited reason.

- As per the WHO data, India, with 8.5% of the total cumulative Covid cases, ranked second after the US with 15.8% of cases.

- Time needed to recover: Taking the actual growth rate of (-) 6.6% for 2020-21, 8.9% for 2021-22 and assuming growth rate of 7.2% for 2022-23 and 7.5% beyond that, India is likely to take another 13 years (by 2034-35) to overcome the losses incurred due to the Covid pandemic.

- The blueprint of reforms:

- Revive and reconstruct: It revolves around seven wheels of economic progress -

- Aggregate demand,

- Aggregate supply,

- Institutions, intermediaries and markets,

- Macroeconomic stability and policy coordination

- Productivity and technological progress

- Structural change

- Sustainability

- Suggested structural reforms: It includes

- Enhancing access to litigation free low-cost land.

- Raising the quality of labour through public expenditure on education and health and the Skill India Mission.

- Scaling up R&D activities with an emphasis on innovation and technology.

- Creating an enabling environment for start-ups and unicorns.

- Rationalisation of subsidies that promote inefficiencies.

- Encouraging urban agglomerations by improving the housing and physical infrastructure.

- A policy ecosystem for Industrial revolution 4.0 and committed transition to a net-zero emission target.

- Reforming banking system:

- Capital infusion should not become a substitute for better governance and risk controls.

- The Public Sector Banks (PSBs) should not be dependent on the government for recapitalisation.

- This will be an important precondition to achieve greater privatisation of the sector.

- To increase the competition in the banking sector and to introduce innovation, the RBI’s ‘on tap’ licensing policy for universal and small finance banks may be used effectively.

- Preconditions for these reforms:

- A feasible range of GDP growth in India (6.5 - 8.5%). Reducing general government debt to below 66% of GDP over the next five years is important to secure India’s medium-term growth prospects.

- Timely rebalancing of monetary and fiscal policies.

- Price stability.

- How are other countries handling the situation?

- No-Covid policy in China, Hong Kong and Bhutan.

- Relatively open borders and removal of internal restrictions in Denmark and the UK.

- Challenges ahead:

- The pandemic is not yet over: A fresh wave of Covid has hit China, South Korea and several parts of Europe.

- Ongoing Russia-Ukraine conflict: Exacerbated dangers to global and domestic growth as a result of rise in commodity prices and global supply chain disruptions.

- Way ahead for India:

- The capital expenditure push in the next Budget can help achieve sustainable high growth.

- This will also enhance productive capacity, crowding in private investment and strengthening aggregate demand.