Why in News?

Pulses posted an annual retail inflation of 16.84% in April 2024, making it more painful for the consumers, given the fact that pulses are hardly sold through the public distribution system (PDS).

Food inflation pressures during an El Niño and election year have undone the nation's progress toward near pulse self-sufficiency.

What’s in Today’s Article?

- Pulses Production in India

- The Current Prices of Pulses as per the Department of Consumer Affairs

- Cause and Effect of the Inflation in Pulses

- Sign of Relief and Challenges Ahead

Pulses Production in India:

- Pulses are the major sources of protein in the diet and these are grown in all three seasons (Kharif: Arhar, Urad, Moong; Rabi: Gram, Lentil, Pea; Summer: Greengram, Blackgram and Cowpea) in India.

- India, with over 35 Mha pulses cultivation area, is the largest pulses producing country in the world.

- It ranks first in area and production with 37% and 29% respectively. During 2021-22 our productivity at 932 kg/ha, has also increased significantly over the last 5 years.

- The Department of Agriculture & Farmers Welfare is implementing the National Food Security Mission (NFSM)-Pulses.

- It aims to increase production through area expansion and productivity enhancement in all the districts of 28 States and 2 UTs (J&K and Ladakh) of the country.

- In order to increase the productivity potential of pulses crops in the country, the ICAR is undertaking basic and strategic research on these crops.

- Further to ensure remunerative prices to farmers, the Government implements an umbrella scheme PM Annadata Aay Sanrakshan Abhiyan (PM-AASHA).

- It comprises Price Support Scheme (PSS), Price Deficiency Payment Scheme (PDPS) and Private Procurement Stockist Scheme (PPSS).

- It ensures Minimum Support Price (MSP) to farmers for their produce of notified oilseeds, pulses and copra.

The Current Prices of Pulses as per the Department of Consumer Affairs:

- Chana (chickpea): It is the cheapest available pulse at an average all-India modal (most-quoted) price of was Rs 85 per kg on May 23, as against Rs 70 a year ago.

- Arhar/tur (pigeon pea): The corresponding price rise of this has been even more from Rs 120 (a year ago) to Rs 160 per kg now.

- Urad (black gram) and Moong (green gram): The prices have increased from Rs 110 to Rs 120 per kg for both.

- Masoor (red lentil): It is the only pulse whose modal retail price has actually eased from Rs 95 to Rs 90 per kg.

Cause and Effect of the Inflation in Pulses:

- Cause - Decline in domestic pulses production: From 27.30 million tonnes (mt) in 2021-22 and 26.06 mt in 2022-23 to 23.44 mt in 2023-24, as a result of irregular/deficient monsoon caused by El Niño and winter rain.

- Farmers (especially in Karnataka, Maharashtra, Andhra Pradesh and Telangana) planted less area due to irregular/deficient rainfall.

- The two pulses (chana and arhar) to register the highest inflation have both seen sharp output falls.

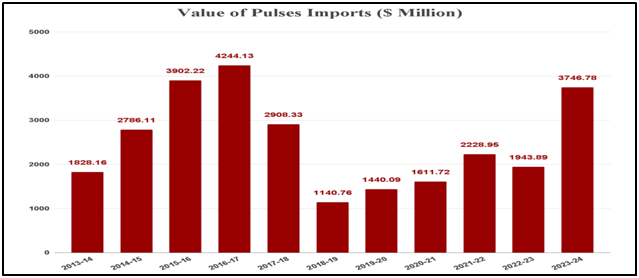

- Effect - Surge in imports:

- Renewed food inflation pressures have forced the Central government to phase out tariffs and quantitative restrictions (QR) on imports of most pulses.

- As a result, India’s pulses imports - valued at $3.75 billion in 2023-24 (April-March), were the highest since the record $3.90 billion and $4.24 billion of 2015-16 and 2016-17.

- In quantity terms, import of major pulses totaled 4.54 mt in 2023-24, up from 2.37 mt and 2.52 mt in the preceding two fiscals.

- Effect - Reversal of the relative self-sufficiency achieved by the country:

- Domestic pulses production rose from 16.32 mt to 27.30 mt between 2015-16 and 2021-22, as a result of government incentivising farmers to grow pulses.

- These policy measures of incentivising farmers included MSP-based procurement and levying of duties on imports.

- Domestic production further rose with the development of short-duration (50-75 day) chana and moong varieties, which can be grown with little to no irrigation by utilising the remaining soil moisture from prior crops.

- The allowed planting of as many as four crops a year: kharif (post-monsoon), rabi (winter), spring and summer.

Sign of Relief and Challenges Ahead:

- La Niña: According to global climate projections, El Niño is expected to shift into a neutral phase next month, and there's even a chance of La Niña, which is linked to abundant rainfall in the subcontinent.

- Unstable domestic supply:

- From this year's crop, the government agencies have procured very little chana, as opposed to 2.13 mt in 2023 and 2.11 mt in 2022.

- Till March 31, 2025, the government has already approved duty-free imports of urad, masoor, desi chana, and arhar/tur.

- Import of cheaper substitutes:

- A less expensive alternative to chana are yellow/ white peas, which can be imported for between Rs 40 and Rs 41 per kg.

- Similarly, masoor dal is replacing arhar or tur in many eateries to make sambar.

- Imports of these pulses from Russia, Australia and Canada, are anticipated to increase more than urad and arhar/tur from East Africa and Myanmar.