Why in News?

- Recently, the Reserve Bank of India (RBI) has cautioned against the reintroduction of the Old Pension Scheme (OPS) by some states.

What’s in today’s article:

- About OPS (Purpose, Features, Drawbacks)

- About NPS (Purpose, Features, Benefits, Comparison with OPS)

- News Summary

What is the Old Pension Scheme (OPS)?

- OPS offers pensions to government employees on the basis of their last drawn salary. 50% of the last drawn salary.

- The attraction of the Old Pension Scheme lay in its promise of an assured or ‘defined’ benefit to the retiree. It was hence described as a ‘Defined Benefit Scheme’.

- Eg., if a government employee’s basic monthly salary at the time of retirement was Rs 10,000, she would be assured of a pension of Rs 5,000.

- Also, like the salaries of government employees, the monthly pay-outs of pensioners also increased with hikes in dearness allowance or DA announced by the government for serving employees.

- The OPS was discontinued by the Central government in 2003.

What were the concerns with the OPS?

- The main problem was that the pension liability remained unfunded — that is, there was no corpus specifically for pension, which would grow continuously and could be dipped into for payments.

- The Government of India budget provided for pensions every year; there was no clear plan on how to pay year after year in the future.

- The ‘pay-as-you-go’ scheme created inter-generational equity issues — meaning the present generation had to bear the continuously rising burden of pensioners.

What is New Pension Scheme (NPS)?

- As a substitute of OPS, the NPS was introduced by the Central government in April, 2004.

- This pension programme is open to employees from the public, private and even the unorganised sectors except those from the armed forces.

- The scheme encourages people to invest in a pension account at regular intervals during the course of their employment.

- After retirement, the subscribers can take out a certain percentage of the corpus.

- The beneficiary receives the remaining amount as a monthly pension, post retirement.

- Nodal agency: Pension Fund Regulatory and Development Authority (PFRDA)

Eligibility:

- Any Indian citizen between 18 and 60 years can join NPS.

- NRIs (Non-Residential Indians) are also eligible to apply for NPS.

Permanent Retirement Account Number (PRAN):

- Every NPS subscriber is issued a card with 12-digit unique number called Permanent Retirement Account Number or PRAN.

Minimum contribution in NPS:

- The subscriber has to contribute a minimum of Rs. 6,000 in a financial year.

- If the subscriber fails to contribute the minimum amount, his/her account is frozen by the PFRDA.

Who manages the money invested in NPS?

- The money invested in NPS is managed by PFRDA-registered Pension Fund Managers.

- At the moment, there are eight pension fund managers.

What is the Difference between NPS and OPS?

- The Old Pension Scheme is a pension-oriented scheme. It offers regular pensions to employees during retirement. The pension amount is 50% of the last drawn salary by the employee.

- Thus, in OPS, the pension amount is constant.

- On the other hand, the National Pension Scheme is an investment cum pension scheme.

- NPS contributions are invested in market-linked securities, i.e., equity and debt instruments.

- Therefore, NPS doesn’t guarantee returns.

- However, the investments, in NPS, are volatile and hence have the potential to generate significant returns.

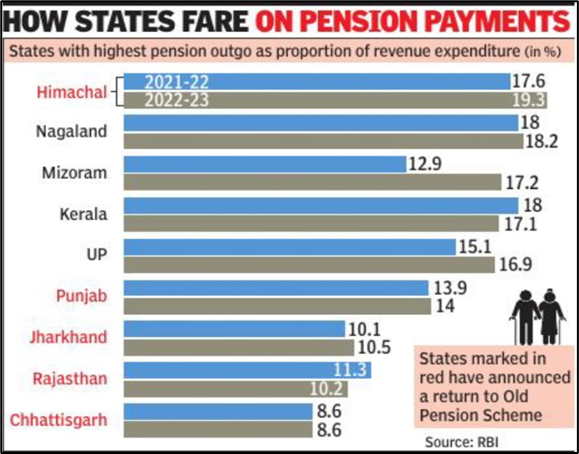

News Summary:

- The RBI has red-flagged the return to the Old Pension Scheme (OPS) by some states as a major concern on the sub-national fiscal horizon.

- The RBI said “by postponing current expenses to the future, states risk accumulation of unfunded pension liabilities in the coming years”.

- Several states, including Himachal Pradesh, Jharkhand, Punjab, Chhattisgarh and Rajasthan have announced a return to the OPS, promising retired government employees 50% of the last pay drawn as the monthly pension.

- Several economists have criticised the move by the states. In several cases, the pension outgo is already high (see graphic below).