Why in News?

Household net financial savings to GDP ratio in India have declined due to increased borrowing and structural shifts rather than a mere change in savings pattern.

Hence, there is a need for macroeconomic policies to support household income growth to reduce financial stress on individuals and stabilise the macroeconomy.

What’s in Today’s Article?

- How the Debate on India’s Declining Household Savings Emerges?

- Declining Household Savings is Not a Mere Change in Savings Pattern

- What is the Argument of the CEA?

- What is the Problem with the CEA’s Argument?

- Is a Higher Household Debt-to-Income Ratio a Sign of a Structural Change?

- What are the Macroeconomic Challenges Highlighted by this Structural Change?

How the Debate on India’s Declining Household Savings Emerges?

- According to a news article, there has been a drastic fall in household net financial savings to GDP ratio during 2022-23 in India on account of a higher borrowing to GDP ratio.

- The higher borrowing to GDP ratio largely reflected a household’s need to finance greater interest payment commitments, leading to an increase in financial distress of the household.

- In response to this article, the Chief Economic Advisor (CEA) to the Government of India has interpreted this trend as a mere shift in the composition of household savings.

- According to the CEA, households incur greater borrowing (or reduce net financial savings) solely to finance higher physical savings (investment).

- Therefore, there is the need to find inconsistencies in this interpretation of the CEA and highlight some signs of structural shifts in the Indian economy.

Declining Household Savings is Not a Mere Change in Savings Pattern:

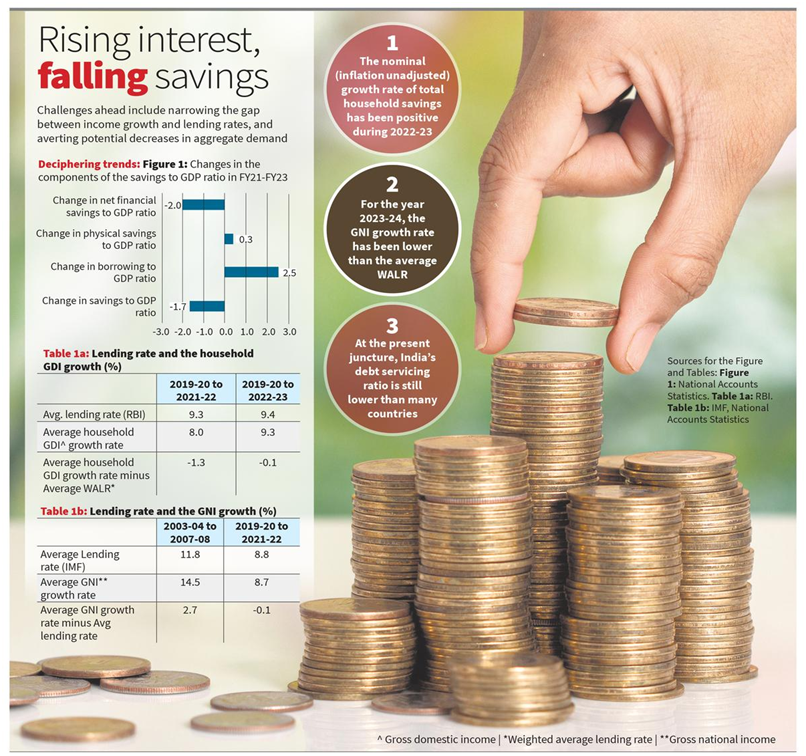

- The household savings to GDP ratio is the sum of its net financial savings to GDP ratio, physical savings to GDP ratio and gold and ornaments.

- A mere shift in the composition of savings would have kept the overall household savings to GDP ratio unchanged.

- This is because the lower net financial savings to GDP ratio or higher borrowing to GDP ratio is compensated by higher physical savings to GDP ratio.

- However, the trends depict another picture.

- The net financial savings to GDP ratio declined by 2.5 percentage points, whereas the physical savings to GDP ratio increased only by 0.3 percentage points.

- The household borrowing to GDP ratio increased by 2 percentage points, significantly more than the increase in the physical savings to GDP ratio.

- With the gold savings to GDP ratio remaining largely unchanged, the household savings to GDP ratio declined by 1.7 percentage points.

What is the Argument of the CEA?

- The CEA’s response is based on the analysis of absolute nominal (inflation unadjusted) numbers of household total savings.

- The nominal value of a household’s total savings has increased, as the nominal value of physical savings has increased more than the fall in nominal value of net financial savings.

What is the Problem with the CEA’s Argument?

- This trend merely shows that the nominal growth rate of total household savings has been positive during 2022-23.

- However, this trend neither addresses the historic fall in net-financial savings to GDP ratio nor invalidates the explanation of the higher borrowing to GDP ratio.

Is a Higher Household Debt-to-Income Ratio a Sign of a Structural Change?

- The share of interest payment in household income is the product of interest rate and debt-income ratio.

- The recent period has been associated with a sharp rise in both these variables.

- The debt-income ratio of the household is increasing due to -

- A higher net borrowing-income ratio of the household, where net borrowing is the difference between total borrowing and interest payments.

- The increase in interest rates and reduction in nominal income growth rate of households. The phenomenon is known as “Fisher dynamics”.

- The key structural feature that has emerged in the post-COVID period is that the nominal income growth rate has often been lower than the weighted average lending rate.

- However, the good news is that India’s debt servicing ratio (at present) is still lower than that of many countries.

- Debt servicing ratio is a comparison of one's debt commitment to his/her income.

What are the Macroeconomic Challenges Highlighted by this Structural Change?

- With the emergence of the Fisher dynamics, there are two unique challenges that confront the Indian economy.

- The first challenge pertains to decreasing the gap between interest rate and income growth, which can quickly push up household’s interest payment burdens.

- The second challenge is preventing aggregate demand from declining in the face of household debt obligations and rising interest rates.

- These challenges point towards the need to include a macroeconomic policy to stimulate and support household income growth and stabilise the economy.