Why in News?

The Central Board of the Reserve Bank of India (RBI) approved a highest-ever surplus transfer/ dividend of Rs 2.11 lakh crore to the Central government for the accounting year 2023-24.

The transferable surplus for the year (2023-24) has been arrived at on the basis of the Economic Capital Framework (ECF).

What’s in Today’s Article?

- What is the Economic Capital Framework (ECF)?

- What is the Surplus Distribution Policy of the Revised ECF?

- Surplus Transfer by the RBI to the Central Government

- What Led to the Higher Dividend Transfers to the Government?

What is the Economic Capital Framework (ECF)?

- Meaning:

- The ECF provides a methodology for determining the appropriate level of risk provisions and profit distribution to be made under Section 47 of the RBI Act 1934.

- As per this provision, the central bank is required to pay the balance of its profits to the central government after making provision for bad and doubtful debts, depreciation in assets, and contributions to staff.

- Old ECF:

- The old ECF was developed in 2014-15, and was operationalised in 2015-16.

- In order to propose a suitable surplus distribution policy, the RBI had constituted an Expert Committee (Chair: Dr Bimal Jalan) to review the current economic capital framework, in 2018.

- Revised ECF: The RBI adopted (on August 26, 2019) a revised ECF as per the recommendations of the Bimal Jalan Committee and this framework may be reviewed every five years.

What is the Surplus Distribution Policy of the Revised ECF?

- The previous surplus distribution policy targets only the total economic capital.

- Economic capital of a central bank includes its capital, reserves, risk provisions and revaluation balances.

- However, the Expert Committee recommended that the target should also include realised equity.

- Realised equity is the component of RBI’s economic capital comprising its capital, reserve fund and risk provisions.

- The Committee had recommended that -

- The total economic capital should be maintained between 20.8% to 25.4% of the RBI’s balance sheet.

- The risk provisioning under the Contingent Risk Buffer (CRB) should be maintained within a range of 5.5-6.5% of the RBI’s balance sheet.

- The risk provisioning made from economic capital to cover monetary, fiscal stability, credit and operation risks is cumulatively referred to as the CRB.

- The CRB is the country’s savings for a financial stability crisis, which has been consciously maintained with the RBI in view of its role as Lender of Last Resort.

- If the realised equity is above the required levels, the entire net income of RBI will be transferred to the government.

- If it is lower, risk provisioning will be made to the necessary extent and only the residual net income will be transferred.

Surplus Transfer by the RBI to the Central Government:

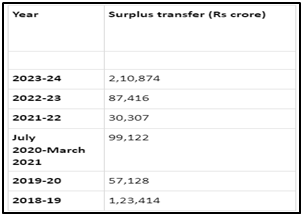

- The Central Board of Directors of the RBI approved the transfer of Rs 2,10,874 crore as surplus to the Central Government for the accounting year 2023-24.

- The latest transfer by the central bank is more than double the ₹87,416 crore that the RBI had transferred in FY23.

- The RBI Board also decided to increase the CRB to 6.50% for 2023-24, from 6% in the previous year, as the economy remains robust and resilient.

- In the Interim Budget for FY2025, the government had set an ambitious target of bringing down the fiscal deficit target to 5.1% of GDP in FY25 from 5.8% of GDP in FY24.

- The bumper dividend payout is likely to help ease FY25 fiscal deficit by around 0.2% of the GDP amid potential shortfall in disinvestment receipts and moderate tax collection growth than budgeted.

What Led to the Higher Dividend Transfers to the Government?

- The higher dividend (representing additional fiscal revenue of 0.4% of GDP) to the government is partly because of an increase in the revenue of the RBI from the variable repo rate (VRR) auctions.

- These auctions were conducted by the RBI last year to provide banks funding support amid tight liquidity conditions.

- The revaluation gains on forex reserves, higher interest rates on domestic and foreign securities and significantly higher gross sales of foreign exchange can also be attributed to the RBI’s higher dividend to the government.

- The RBI normally pays the dividend from the surplus income it earns on investments and valuation changes on its dollar holdings and the fees it gets from printing currency.

- The rupee’s depreciation against the dollar has also led to the surplus transfer.