Context

- The article analyses the budget provisions from the perspective of meeting the goals of growth and stability, as the two must go together for sustained growth over the medium term, tackling many of India’s socioeconomic problems.

Budgetary Support to Ensure Growth

- Growth is dependent upon the size of government expenditure and its revenue and capital components.

- The capital expenditure represents expenditure incurred for the purpose of acquiring a fixed asset which is intended to be used over long term for earning profits.

- The revenue expenditure, on the other hand, represents government spending that does not result in production of assets, like on salary, wages, pension, subsidy and interest payments.

- Recent Budget estimates: Government expenditure is budgeted to grow at 7.5% while nominal GDP growth is estimated to fall from 15.4% in 2022-23 to 5% in 2023-24.

- Thus, the total expenditure relative to GDP is shown to fall from 15.3% in 2022-23 (RE) to 14.9% in 2023-24 (BE).

- The composition of government expenditure, however, would be growth positive. Real growth in 2023-24 may be a little above 6%.

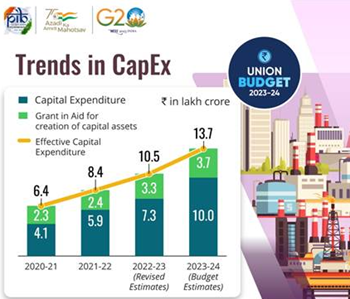

- Allocation of revenue vis-à-vis capital expenditure: Increase in the Centre’s capital expenditure is budgeted at 37% while that in revenue expenditure is only 1.2%.

- According to RBI estimates (2019, 2020), the multiplier associated with central government capital expenditure is 2.45, while that for revenue expenditure is 0.45.

- However, the investment expenditure by central public sector undertakings (PSUs) is budgeted to fall by 0.2% points.

- Expected boost in State’s capital assets creation: The State capital expenditures may increase as a result of central grants to the States meant for capital asset creation amounting to 1.2% of GDP.

- Also, augmentation of States’ fiscal deficit to GDP ratio to 3.5%, and the facility of 50 years of interest-free loans for creating capital assets in 2023-24 could further boost infrastructure creation.

- Other avenues of growth: Growth may also be stimulated indirectly due to an increase in private disposable incomes following tax slab adjustments applicable to the new income tax regime.

- Basic exemption limit is hiked from Rs 2.5 lakh to Rs 3 lakh and rebate under section 87A of IT Act has been hiked from Rs 5 lakh to Rs 7 lakh in the Budget 2023-24.

Flexible Budget Amid External Shocks

- The global uncertainties like three continuous COVID-19 waves, ongoing Russia Ukraine conflict necessitated additional flexibilities in terms of expenditure management and fiscal consolidation.

- For example, Fiscal deficit jumped to a record 9.3% in 2020-21, from 4.6% the previous year on account of pandemic-linked spending.

- Operational targets under FRBM Act: As per amended Fiscal Responsibility and Budget Management (FRBM) Act, 2018, the Centre is mandated to take appropriate steps to limit its fiscal deficit to 3% of GDP by March 31, 2021

- The mandated target pertains to the Centre’s debt-GDP ratio to be brought down to 40%.

- The Centre is also required to state the reasons if there is a deviation from the fiscal deficit-GDP ratio of 3%.

- The fiscal deficit in Budget 2023-24 is projected to be 9% of GDP against the 6.4% in the revised estimates for 2022-23.

- Missing medium-term GDP growth forecasts: In the medium-term fiscal policy cum Fiscal Policy Strategy Statement (MTFP), the Centre attributed the deviation of the budgeted 5.9% fiscal deficit-GDP ratio to external economic conditions.

- For this reason, the Centre has also not provided the medium-term GDP growth forecasts.

- The MTFP statement also does not indicate the year by which the government aims to reach the mandated debt-GDP target of 40%.

- No fixed deadline for fiscal deficit target: The Centre has also not indicated the year by which it envisages reaching a fiscal deficit level of 3% of GDP.

- Instead, it indicated to reduce fiscal deficit to below 4.5% of GDP by 2025-26, thus calling for a steeper adjustment of 0.7% points each in the next two years.

- Accordingly, the fiscal deficit is expected to decrease to 5.9% in 2023–2024.

- It can hence be inferred that it might require another two to three years for reaching a level of 3%.

- However, even by this time, the mandated debt-GDP ratio of 40% would not be reached.

- Liability burden of Centre: The Centre’s debt-GDP level net of liabilities on account of investment in special securities of states under the National Social Security Fund (NSSF) is budgeted to increase from 55.7% in 2022-23 (RE) to 56.1% in 2023-24 (BE).

- This increase is expected as the primary deficit to GDP ratio is indicated at 2.3% in 2023-24.

- Higher Centre’s debt-GDP ratio: The high level of Centre’s debt-GDP ratio is for interest payments relative to revenue receipts, which is budgeted at 41% in 2023-24.

- This reduces, significantly, the space for primary expenditure in the Centre’s budget.

Augmenting Private Investment

- The boost of private investment relative to GDP needs to be ensured for raising growth in the medium term.

- This will require enough investible resources to be left for the private sector after the public sector’s pre-emptive claim on these resources.

- Total investible reserves: At present, total investible resources, consisting of financial savings of the household sector amounting to about 8% of GDP and net foreign capital inflows amounting to 2.5% of GDP, may be estimated at 10.5% of GDP.

- The central and State fiscal deficits considered together also may amount to 9.4% of GDP in 2023-24.

- This implies that only 1.1% is available for the private sector and the non-government public sector.

- Shrinked scope for private investment: The investment of the Centre’s PSUs themselves amount to 1.1% of GDP in 2023-24, leaving little scope for State PSUs and the private sector.

- This creates a non-compliant environment for interest rate reduction as borrowing beyond the available investible resources by the government could lead to inflation.

Conclusion

- The government is trying to steer economic growth through capital expenditure (capex) as it will boost private investment.

- For example, the ratio of capital expenditure to Fiscal Deficit (Capex-FD) is estimated at 56.0% in BE 2023-24 as compared to 41.5% in RE 2022-23 and 37.4% in FY 2021-22.

- The Capital investment outlay increase by 33% to Rs. 10 lakh crores (roughly twice the absolute amount spent in 2021-22), depicting desire for “crowding-in” of private sector investment asserting “boost infrastructure expansion to boost growth” dictum.

- Hence, a stronger fiscal consolidation road map over the medium term is needed to address the dilemma related to reduction in the fiscal deficit and economic growth recovery.