Why in News?

The Ministry of New and Renewable Energy (MNRE) reimposed its mandate requiring solar projects to source (photovoltaic [PV]) modules exclusively from a government-approved list of domestic manufacturers starting April 1.

This comes amid concerns over market concentration in India’s solar PV module industry and its potential to drive-up household electricity tariffs.

What’s in Today’s Article?

- Government Initiatives to Bolster Domestic Clean Technology Manufacturing

- Implications of Market Concentration in India’s Solar PV Module Industry

- India’s Renewable Energy Prospects

Government Initiatives to Bolster Domestic Clean Technology Manufacturing:

- The ALMM (Approved List of Model Manufacturers):

- Issued by the MNRE in 2021, it mandates all government-assisted or associated solar projects to use only enlisted modules, effectively barring the use of imported modules in most projects.

- The order aims to enhance energy security by reducing import dependence.

- The order was reimposed recently because the enlisted capacity of around 50 GW is believed to be sufficient and the duty-free import of solar modules from ASEAN countries is detrimental to domestic producers.

- The Production Linked Incentive (PLI) scheme for solar PV modules: Till now, the MNRE has announced incentives for 48.3 GW of module manufacturing capacities under the PLI scheme.

Implications of Market Concentration in India’s Solar PV Module Industry:

- Positive:

- The BCD (Basic Custom Duty of 40% on solar module imports) will help grow the consumption demand of domestically manufactured products.

- Manufacturers anticipate a multifold increase in solar panel installations due to the PM-Surya Ghar Muft Bijli Yojana's goal of installing one crore household rooftop solar panels.

- Furthermore, solar panel manufacturers are also hoping for a policy change in European countries on the lines of the US which may open the European market for India.

- Negative:

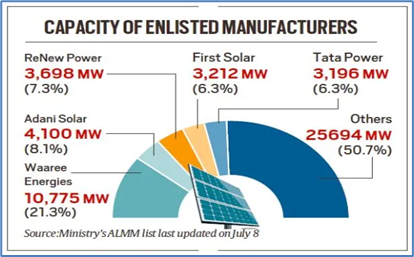

- Companies linked to just five manufacturers control nearly half of the current capacity listed on the ALMM.

- Domestic solar modules are now 90% more expensive than imports, with prices reaching 18 cents per watt compared to 9.1 cents for imported modules.

India’s Renewable Energy Prospects:

- Current situation:

- It should be mentioned that India is the 3rd largest energy consuming country and stands 4th for total renewable power capacity additions.

- As of (May) 2024, India’s renewable energy capacity stands at 195.01 GW with solar power capacity of 85.47 GW, wind power of 46.65 GW, small hydro power of 5 GW and large hydro power of around 46 GW.

- At COP26 India announced its plan to achieve the target of 500GW of non-fossil fuel-based energy by 2030.

- Future projections:

- India’s power consumption is growing at around 10%-12% per annum resulting in an additional power demand of 20-25 GW annually.

- This increasing demand combined with the government initiatives may create a multi fold increase in the demand for solar installations.

- Challenges:

- In order to reach the 2030 target, India needs to add about 44 GW annually, requiring an investment of US$ 190-215 billion over seven years.

- According to the Ministry of Commerce & Industry data, the total solar capacity installed in FY 24 was around 15 GW this far.

- Land acquisition and infrastructure development to establish an efficient transmission network are the major challenges that the industry and the government need to address.

- India’s per capita power consumption is only around one third of the global average.