Why in news?

The GST Council of India introduced e-invoicing (electronic invoicing) in a phased manner to standardize business-to-business (B2B) invoice reporting to the GST portal.

There were no predefined formats. Hence, a uniform structure was developed in consultation with trade bodies and the Institute of Chartered Accountants of India.

Over time, several modifications have been made to the e-invoicing regulations to enhance compliance and efficiency.

What’s in Today’s Article?

- GST E-Invoicing: Overview & Process

- Advantages of GST E-Invoicing

- New GST E-Invoicing Rules from April 1, 2025

GST E-Invoicing: Overview & Process

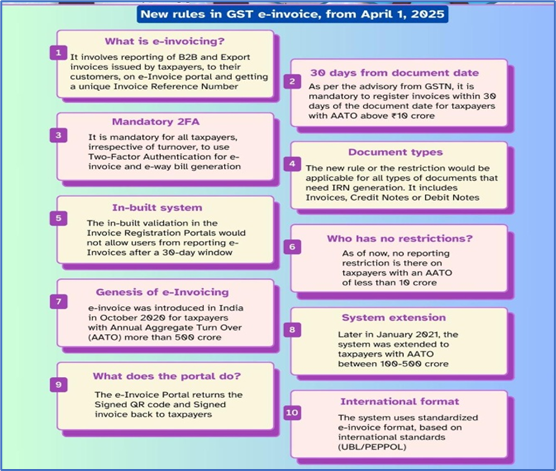

- GST e-invoicing is a system where B2B and export invoices are reported to the Union Government’s e-invoice portal for validation.

- Each invoice receives a unique Invoice Reference Number (IRN).

- However, invoices are not generated by the government but are created by taxpayers in their own systems and then reported.

- The system enables seamless electronic data exchange through API integration.

- Approval & Rollout

- Approved in the 37th GST Council meeting in September, 2019.

- Rolled out in a phased manner starting October 2020 for businesses with an Annual Aggregate Turnover (AATO) above ₹500 crore.

- Extended in January 2021 to businesses with AATO between ₹100 crore and ₹500 crore.

- Documents Required for IRN Generation

- GST Invoices

- Credit Notes

- Debit Notes (for B2B supplies and exports)

- Exempted Businesses

- Special Economic Zone (SEZ) units

- Insurance and banking sectors, including NBFCs

- Multiplex cinema admissions

- Goods transport agencies (road transport)

- Passenger transport services

- E-Invoicing Process

- Taxpayers generate invoices using their own accounting/billing/ERP systems.

- The invoices are reported to the Invoice Registration Portal (IRP).

- The IRP validates the invoice and assigns a Unique Invoice Reference Number (IRN) along with a QR code.

- A GST invoice is legally valid only if it contains a valid IRN.

Advantages of GST E-Invoicing

- Automation & Efficiency

- Invoice details are auto-populated into GST return forms and e-way bills, reducing time and manual effort.

- Minimizes disputes and processing costs by ensuring digital storage of all forms.

- Improves payment cycles, enhancing overall business efficiency.

- Standardization & Interoperability

- Uses a digitally verifiable e-invoice format based on international standards.

- Ensures machine readability and uniform interpretation across different platforms.

- Allows taxpayers to seamlessly switch between different portals.

- Fraud Prevention & Compliance

- Reduces fraudulent transactions by providing real-time access to data for tax authorities.

- Helps in curbing tax evasion and malpractice, leading to greater transparency.

New GST E-Invoicing Rules from April 1, 2025

- Mandatory 30-Day Deadline for E-Invoice Reporting

- Businesses with an Annual Aggregate Turnover (AATO) of ₹10 crore and above must report e-invoices to the Invoice Registration Portal (IRP) within 30 days of issuance.

- Earlier, this rule applied only to businesses with AATO above ₹100 crore.

- With the lower turnover threshold, many more businesses must now comply with this rule.

- Stricter Compliance & Penalties

- Currently, businesses delay invoice uploads, causing discrepancies in Input Tax Credit (ITC) claims.

- From April 1, IRPs will block invoice uploads beyond 30 days, rejecting late submissions.

- Non-compliance may lead to penalties and financial consequences.

- Compulsory Two-Factor Authentication (2FA)

- From April 1, all taxpayers, regardless of turnover, must use Two-Factor Authentication (2FA) for e-invoice and e-way bill generation.