Context

- The article examines challenges in the pathway to realise the vision of making India energy independent and decarbonising major sectors of the economy and the role of green hydrogen/National Hydrogen Mission in achieving this vision.

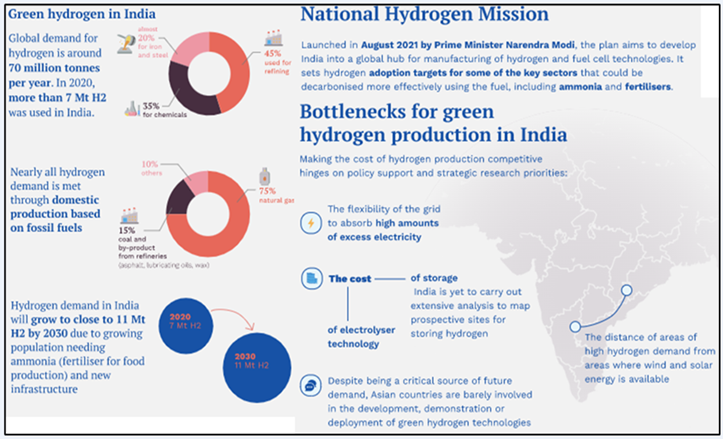

National Hydrogen Mission

- It aims to make India a global production and export hub of green hydrogen.

- It envisages the production capacity of low-cost green hydrogen to touch at least 5 MMT (million metric tonne) per annum by 2030.

- It was launched (in 2023) by the Ministry of New and Renewable Energy (MNRE) with an initial outlay of $2.3 billion over the next five years.

Green Hydrogen

- It is the name given to hydrogen gas that has been produced using renewable energy, such as wind or solar power, which create no GHG emissions.

- For example, hydrogen is produced through water electrolysis and when the electricity used in the water electrolysis is produced from renewables, it is termed as green hydrogen.

Likely Outcomes of Green Hydrogen Mission

- Adding renewable energy capacity of about 125 GW (gigawatt) in the country

- Investments likely to the tune of $100 billion

- Creation of over 6 lakh green jobs

- Savings to the tune of $12.5 billion by cutting fuel imports

- Abatement of nearly 50 MMT of annual GHG emissions

Wide Ranging Benefits Related to Green Hydrogen Mission

- Creation of export opportunities for Green Hydrogen and its derivatives

- Decarbonisation of industrial, mobility and energy sectors

- Reduction in dependence on imported fossil fuels and feedstock

- Development of indigenous manufacturing capabilities

- Development of cutting-edge technologies

4Es Challenges Related to Green Hydrogen

- Electrolyser challenge: According to IEA (International Energy Agency), as of 2021 the global manufacturing capacity of electrolysers stands at 8 GW/year.

- India would need about 60-100 GW of electrolyser capacity, which amounts to almost 12 times the current global production capacity to achieve its 2030 target.

- India currently has launched projects to manufacture electrolysers, but the actual numbers as of today are negligible.

- Also, access to critical minerals such as nickel, platinum group metals and rare earth metals such as lanthanum, yttrium and zirconium could hinder scaling up electrolyser manufacturing capability in India.

- This is because these resources are concentrated in countries such as China, Democratic Republic of Congo (DRC), Australia, Indonesia, South Africa, Chile and Peru, and India has limited processing capabilities in these minerals.

- Energy source challenge: As per current estimates an efficient electrolysis system would require 39 kWh of electricity to produce 1 kg of hydrogen.

- As green hydrogen requires renewable energy as a source of electricity, but so far India has only achieved 119 GW of the 175 GW targeted capacity using solar, wind, bio-power and small hydro.

- In addition to the generation capacity, the transmission capacity that includes a smooth facilitation of cross-border exchange of power between states is a critical requirement.

- End use challenge: Currently, most of the demand for hydrogen comes from the chemical industry to produce ammonia for fertilizers, followed by refining for hydro-cracking and the desulphurisation of fuels.

- It can be a source of heat for industry, such as steel, cement and aluminum production.

- In the transport sector, it can be used as fuel for heavy duty vehicles, aviation and shipping.

- Hence, the conversion efficiency from one form of energy carrier to another in the end use application will determine the scale of green hydrogen’s applicability.

- Endogenous resources challenge: The production of one kg of hydrogen by electrolysis requires around nine litres of water. Thus, a requirement of approximately 50 billion litres of demineralised water supply.

- This is concerning as several parts of India are already severely water-stressed, demanding solutions to be found to cater to this additional water demand.

- While desalination has been suggested to address this challenge, this will have negative repercussions as follows:

- Increasing the physical footprint of the required infrastructure

- Add to competition for land use

- Impact biodiversity

- Create challenges and limitations in the location of electrolysers

Overcoming the Roadblocks

- The electrolyser challenge would entail India setting up large scale manufacturing, building expertise and securing geo-political partnerships for procurement of critical minerals.

- It also demands efforts aimed at improving overall technical and economic viability of electrolysers year-over-year while competing with other global players.

- Tackling energy source challenge would require India to add efficiently and economically close to 100 GW of overall renewable energy capacity per year over the next seven years and make available dispatch corridors and mechanisms.

- To intercept end-use challenge, i.e., produce and store green hydrogen in different forms for later use, it is critical to establish safety standards for storage and transportation.

- This is because hydrogen being a highly combustible and volatile element, its potency in other forms such as ammonia or methanol is only relatively reduced.

- However, this may add to the cost of hydrogen as a fuel.

- The endogenous resources challenge would require the proposed green hydrogen hubs to strike a fine balance between being renewable energy rich and water resource rich.

- It will also entail being close to hydrogen demand (end-use) centres for them to be economically feasible while keeping the additional costs minimum.

Conclusion

- As per IRENA estimates, the hydrogen and its derivatives will account for 12 per cent of global final energy consumption by 2050 (IEA estimate 530MMT), with two-thirds coming from green hydrogen.

- In 2020, the world produced around 90MMT of hydrogen and the current global levelised cost of producing green hydrogen ranges between Rs 250-650/kg ($ 3-8/kg).

- India, which aims to produce green hydrogen in the range of Rs 100-150/kg ($ 1-2/kg) by 2030, will have to address all the challenges listed above as well as coordinate across multiple institutional bodies both public and private in record time.