Why in News?

- The Reserve Bank of India (RBI) has called for extending the ‘pre-packaged’ insolvency resolution process to large borrowers.

- The current process is focused primarily on resolution and requires a majority of creditors to accept a deal before approaching the insolvency court.

What’s in today’s article:

- Background (Meaning of Insolvency, why IBC is needed)

- About IBC 2016 (Purpose, Mandate, Process, Timeframe, etc.)

- News Summary (SARFAESI Act features)

Background:

- In a growing economy like India, a healthy credit flow and generation of new capital are essential, and when a company or business turns insolvent or “sick”, it begins to default on its loans.

- In order for credit to not get stuck in the system or turn into bad loans, it is important that banks or creditors are able to recover as much as possible from the defaulter and as quickly as they can.

- The business can either get a chance, if still viable, to start afresh with new owners, or its assets can be liquidated or sold off in a timely manner.

- This way fresh credit can be pumped into the system and the value degeneration of assets can be minimised.

What is the Insolvency and Bankruptcy Code (IBC)?

- In 2016, at a time when India’s Non-Performing Assets and debt defaults were piling up, the Insolvency and Bankruptcy Code (IBC) code was introduced to overhaul the corporate distress resolution regime in India and consolidate previously available laws to create a time-bound mechanism.

- Insolvency resolution in India took 4.3 years on an average.

- In comparison, countries such as UK and USA took 1 year and 1.5 years, respectively.

- The Insolvency and Bankruptcy Code 2016 was implemented through an act of Parliament.

- The Code aims to promote entrepreneurship, availability of credit and balance the interests of all the stakeholders.

What is the mandate of the IBC?

- When insolvency is triggered under the IBC, there can be two outcomes: resolution or liquidation.

- All attempts are made to resolve the insolvency by either coming up with a restructuring or new ownership plan and if resolution attempts fail, the company’s assets are liquidated.

- Companies have to complete the entire insolvency exercise within 180 days under the IBC.

- For smaller companies including startups with an annual turnover of Rs 1 crore, the whole exercise of insolvency must be completed within 90 days.

Who regulates the IBC proceedings?

- Insolvency and Bankruptcy Board of India has been appointed as a regulator and it can oversee these proceedings.

- IBBI has 10 members; from Finance Ministry, Law Ministry and the RBI.

News Summary:

- The Reserve Bank of India (RBI) has called for extending the ‘pre-packaged’ insolvency resolution process to large borrowers.

- The process refers to an insolvency resolution mechanism where there is an understanding between the debtors and creditors on how to move forward.

- Once two-third of the creditors accept a resolution plan, the parties approach the insolvency court for its implementation.

- The Government had introduced the pre-pack insolvency resolution for MSMEs and other small businesses.

- Speaking in favour of the IBC, the RBI stated that the IBC has helped lenders recover close to 201% of the liquidation value until September 2022.

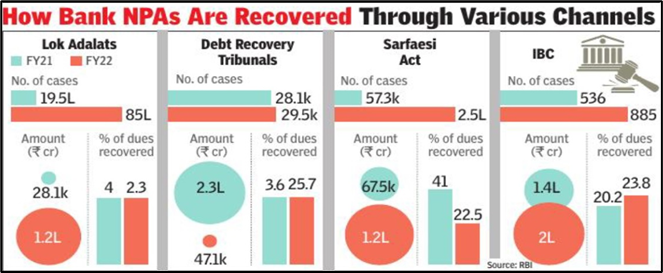

- The RBI has also acknowledged that Debt Recovery Tribunals (DRTs) and the Securitisation & Reconstruction of Financial Assets and Enforcement of Security Interest Act (SARFAESI), 2002 continue to remain as effective as the IBC.

What is the SARFAESI Act?

- Sarfaesi Act was passed by the Parliament on the basis of recommendations made by the Narasimham Committee – II in 1998.

- The committee was formed to review the progress of the implementation of the banking reforms since 1992 with the aim of further strengthening the financial institutions of India.

- The Act Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act came into existence in December, 2002.

- The primary objective of the Act is to enable the Banks and Financial Institutes to recover its money advanced quickly.

Salient Features of the Act:

- The Act empowers the Banks and FI’s to auction the property mortgaged with them to recover such outstanding dues which is not paid for years despite repeated follow-ups’.

- In 2013, the Act was amended to include co-operative banks formally under the definition of banks eligible to use it.

- The Act provides for the establishment of Asset Reconstruction Companies to acquire assets from Banks and other Financial Institutions.

- The ARCs take over a portion of the debts of the bank that qualify to be recognised as NPAs.