In News:

- The Central Board of Direct Taxes (CBDT) has proposed a single income tax return (ITR) form for all taxpayers.

- A draft form has been released, to which all stakeholders can provide inputs up to December 15.

What’s in today’s article:

- About CBDT

- Current ITR system (Number of Forms, Proposal by CBDT, Need for a common form)

About Central Board of Direct Taxation:

- The Central Board of Direct Taxes is a statutory authority functioning under the Central Board of Revenue Act, 1963.

- It is responsible for the administration of direct taxation in India.

- It is administered by the Department of Revenue under the Ministry of Finance.

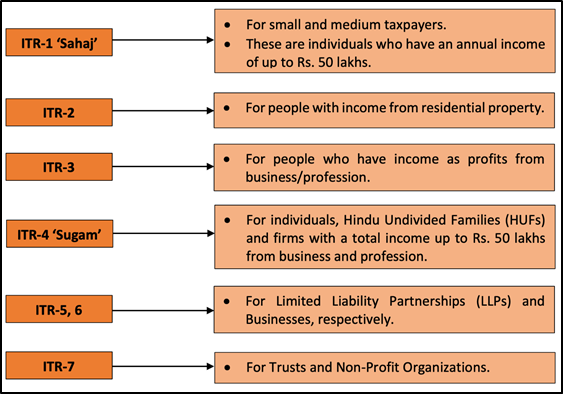

How many kinds of ITR Forms are there now?

- Currently, there are seven kinds of Income Tax Return (ITR) forms which are used by different categories of taxpayers. They are as follows –

How many ITR forms were filed in AY 2022-23?

- The total ITR forms filed for AY 22-23 is about 83 crore.

- Out of 5.83 crore ITRs filed, 50% of these are ITR-1 (2.93 crore), 11.5% are ITR-2 (67 lakh), 10.9% are ITR-3 (63.35 lakh), 26% are ITR-4 (1.54 crore), ITR-5 to 7 (5.5 lakh)

Proposal made by CBDT:

- According to the proposal, all taxpayers, barring trusts and non-profit organisations, will be able to use a common ITR form.

- This common ITR form will include a separate head for disclosure of income from virtual digital assets.

What is the need for a common ITR Form?

- The proposal of having a common ITR Form is aimed at making it easier for citizens for file returns, and also to considerably reduce the time taken for the job by individuals and non-business-type taxpayers.

- With a common ITR form, the taxpayers will not be required to see the schedules that do not apply to them.

- It intends the smart design of schedules in a user-friendly manner with a better arrangement, logical flow, and increased scope of pre-filling.

- It will also facilitate the proper reconciliation of third-party data available with the Income-Tax department vis-à-vis the data to be reported in the ITR to reduce the compliance burden on the taxpayers.