Why in News?

Amid challenges in the fertilizer sector, such as shortages in di-ammonium phosphate (DAP) and limited investments in manufacturing, India's urea industry has achieved significant progress.

Domestic production has risen considerably, reflecting efforts toward the central government's goal of atma nirbharta (self-reliance).

What’s in Today’s Article?

- Overview of Fertiliser Sector in India

- What is Urea Fertilizer?

- Rising Domestic Urea Production

- Greenfield Projects and Efficiency

- Make vs. Buy Debate

- Strategic Shift and Policy Recommendations

- Conclusion

Overview of Fertiliser Sector in India:

- The Economic Survey 2023-24 states that the Indian Agriculture sector provides livelihood support to about 42.3% of the population and has a share of 18.2% in the country’s GDP at current prices.

- Fertilizers, water and seeds are vital inputs for achieving higher agricultural production in the country.

- Government has undertaken various efforts during the last decade due to which the total fertilizer production has increased from 385.39 million tonnes (mt) in 2014-15 to 503.35 mt in 2023-24.

- Several measures were undertaken by the Government to increase the total fertilizer production in the country.

- Urea Subsidy Scheme,

- New Urea Policy 2015,

- Nutrient based Subsidy scheme, etc.

- Besides, it also promotes sustainable methods such as the use of alternative fertilizers viz., Nano Urea, Nano DAP and organic fertilizer in the country.

What is Urea Fertilizer?

- It is a nitrogen-rich fertilizer (46% nitrogen) used to promote crop growth and development.

- It's a low-cost fertilizer. Its high nitrogen content makes transportation and storage less expensive.

- Urea is absorbed by plants directly or converted to ammonia and carbon dioxide by soil microorganisms.

- It can also be used as a cattle feed supplement, and has industrial applications, such as in the production of plastics.

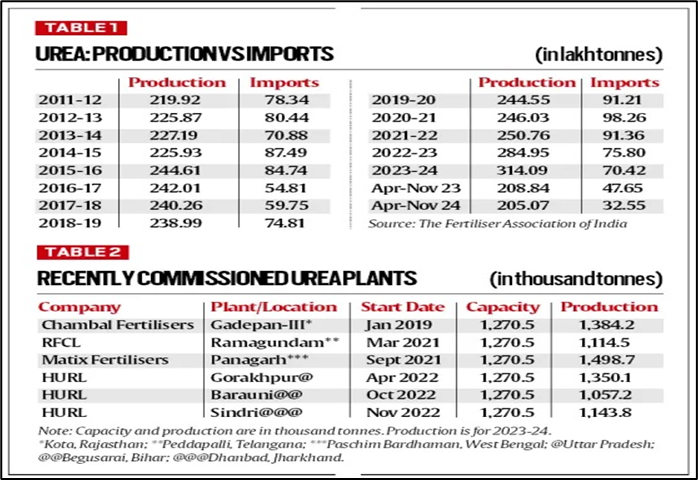

Rising Domestic Urea Production:

- Growth trends: Between 2011-12 and 2023-24, domestic urea production rose from 22 million tonnes (mt) to 31.4 mt, while imports decreased from 7.8 mt to 7 mt.

- Import reduction: The current fiscal recorded a 31.7% drop in imports, potentially reducing imports to below 5 mt, the lowest since 2006-07.

Greenfield Projects and Efficiency:

- New plants:

- Six new urea plants contributed significantly to increased production, with a combined output of 7.55 mt in 2023-24.

- Investments ranged from Rs 6,000-8,600 crore per plant.

- Plants include those by HURL, Chambal Fertilisers, Matix Fertilisers, and RFCL.

- Energy efficiency:

- New plants consume about 5 giga-calories (GCal) per tonne, compared to 5.5-6.5 GCal for older units.

- The Matix Fertiliser plant in Panagarh (West Bengal) emerged as the most energy-efficient, with 4.856 GCal/tonne consumption.

- Regional focus: These plants cater to “new Green Revolution” areas like Eastern UP, West Bengal, Bihar, Jharkhand and Telangana, providing a 20% market share in Eastern India.

- Older units such as the National Fertilizers Ltd’s (NFL) Bathinda, Nangal and Panipat, caters to farmers in Punjab and Haryana.

- Upcoming projects: (Talcher Fertilizer Plant)

- Located in Odisha, this Rs 17,080 crore plant will use coal as a feedstock with advanced coal gasification technology.

- Coal blending with petroleum coke aims to maximize indigenous resources.

Make vs. Buy Debate:

- Cost comparison:

- Domestic production costs: $427-$493 per tonne, depending on tax adjustments.

- Imported urea costs: $370-403 per tonne.

- Logistics advantage:

- Transport and bagging costs make imported urea less viable for northern and eastern regions.

- Domestic plants reduce logistical expenses and provide employment and economic activity under the Make-in-India initiative.

Strategic Shift and Policy Recommendations:

- Regional production strategy:

- Focus on increasing production in Northern and Eastern India while optimizing imports for Peninsular India.

- Shut down older, inefficient plants to enhance energy efficiency.

- Rational pricing:

- Urea’s farmgate price has been fixed at Rs 5,360/tonne since 2012, leading to excessive consumption.

- Rational pricing is crucial for balanced fertilizer use and reducing dependency on both production and imports.

Conclusion:

India’s urea industry has made significant strides toward self-reliance with new energy-efficient plants and strategic investments.

However, achieving a sustainable balance between domestic production and imports requires policy interventions in pricing, regional production focus, and the judicious application of fertilizers.