Why in News?

The Reserve Bank of India (RBI) released the Report on Currency and Finance (RCF) for the year 2023-24 with the theme - India’s Digital Revolution.

What’s in Today’s Article?

- India’s Digital Revolution - Highlights of the RCF

- Significance of the Digitalisation in Finance in India

- Challenges Posed by the Digitalisation in Finance

- Remittances in India - Highlights of the RCF

- Way Forward for a Robust Digital Finance Ecosystem in India

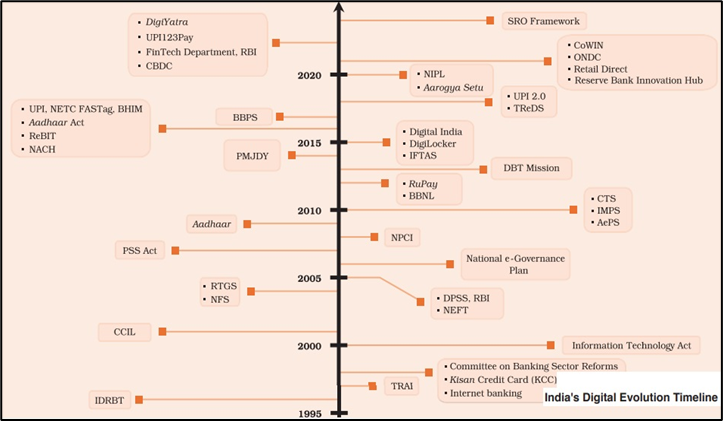

India’s Digital Revolution - Highlights of the RCF:

- India is leading the global digital revolution, emerging as a frontrunner on the back of its robust digital public infrastructure (DPI), rapidly evolving institutional arrangements, and a growing tech-savvy population.

- Globally, India ranks first in biometric-based identification (Aadhaar) and real-time payments volume; second in telecom subscribers; and third in terms of the startup ecosystem.

- The flagship Unified Payments Interface (UPI) has revolutionised the retail payment experience for end users, making transactions faster and more convenient.

- In the digital currency arena, the RBI is at the forefront with pilot runs of the e-rupee, the central bank digital currency (CBDC).

- The digital lending ecosystem is becoming vibrant with initiatives such as the Open Credit Enablement Network, the Open Network for Digital Commerce and the Public Tech Platform for Frictionless Credit.

- FinTechs are collaborating with banks and non-banking financial companies (NBFCs) as lending service providers.

- They are also operating platforms to facilitate digital credit.

Significance of the Digitalisation in Finance in India:

- Paving the way for next-generation banking: For example, loans in the retail segment are being enabled by online payments and innovative credit assessment models with instant disbursements.

- Innovations are making financial markets more efficient, integrated and inclusive: By -

- Improving access to financial services at affordable costs;

- Enhancing the impact of direct benefit transfers (DBTs) by effective targeting of beneficiaries in a cost-efficient manner; and

- Boosting E-commerce through embedded finance.

- On the external front: Digitalisation is driving growth in India’s services exports and lowering remittance costs.

- Transforming DPI as a global public good: For example, the RBI has joined Project Nexus - a multilateral international initiative to enable instant cross-border retail payments by interlinking domestic Fast Payments System (FPS).

- As part of the project, the country’s UPI and FPSs of Malaysia, Philippines, Singapore and Thailand will be interlinked through Nexus.

Challenges Posed by the Digitalisation in Finance:

- Customer protection: It presents challenges related to cybersecurity, data privacy, data bias, vendor and third-party risks.

- Complex products and business models: Emerging technologies can introduce such models with risks that users may not fully understand, including the proliferation of fraudulent apps and mis-selling through dark patterns.

- Human resource challenges: Digitalisation may induce human resource challenges in the financial sector, necessitating strategic investments in upskilling and reskilling.

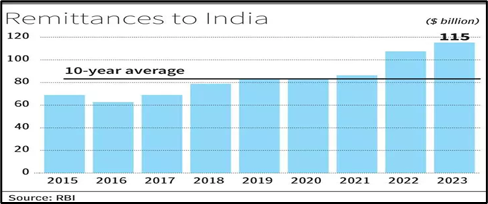

Remittances in India - Highlights of the RCF:

- Highest remittance recipient in the world:

- According to the World Bank, global remittances are estimated to have increased to US$ 857.3 billion in 2023.

- This is led by India (US$ 115.3 billion - accounting for 13.5% of the world total), Mexico (US$ 66.2 billion), China (US$ 49.5 billion) and the Philippines (US$ 39.1 billion).

- The cost of sending remittances globally has decreased over time, with digitalisation playing a key role.

- Trends in India:

- In 2021, more than half of India’s inward remittances were from the Gulf countries, while North America accounted for 22% share.

- The ratio of remittances to GDP for India has gradually increased from 2.8% in 2000 to 3.2% in 2023. It is now above that of gross FDI inflows to GDP ratio (1.9% in 2023), providing strength to India’s external sector.

- Future projections:

- Going forward, India is poised to be the world’s leading supplier of labour as its working-age population is expected to rise until 2048, while it has started dwindling for major advanced economies.

- This will propel remittances to around $160 billion in 2029 from $115 billion in 2023, and propel skill upgradation of the workforce.

Way Forward for a Robust Digital Finance Ecosystem in India:

- Regulatory and supervisory frameworks must scale up and become more sophisticated to balance financial stability, customer protection and competition.

- For example, the Government of India has introduced the Digital Personal Data Protection (DPDP) Act 2023 to fortify the protection of personal data in the rapidly evolving digital landscape.

- The goal is to balance effective regulation with fostering financial innovations in a safe, robust and trustworthy ecosystem.