Why in News?

A nine-judge Bench of the Supreme Court of India (SC), in an 8:1 decision, ruled that states have the authority to impose taxes not only on alcoholic beverages but also on 'industrial' alcohol. This decision expands states' revenue-generating capabilities, with significant implications for both taxation and federalism.

What’s in Today’s Article?

- Background of the Dispute of Taxing Industrial Alcohol

- The SC’s Verdict on Taxing Industrial Alcohol

- Implications of SC’s Verdict on Taxing Industrial Alcohol

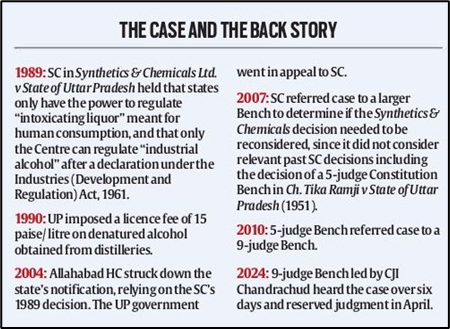

Background of the Dispute of Taxing Industrial Alcohol:

- Background:

- Why is the taxation of industrial alcohol controversial?

- Overlapping constitutional entries:

- The dispute involved two entries in the Seventh Schedule of the Constitution.

- Entry 8 of List II (State List) gives states authority over intoxicating liquors, while Entry 52 of List I (Union List) grant the Centre the power to regulate industries.

- Additionally, Entry 33 of List III (Concurrent List) grants the Centre authority over any industry that Parliament has legally determined to be in the public interest.

- Centre claims its jurisdiction:

- According to the central government, industrial alcohol falls under its jurisdiction due to its inclusion in the Industries (Development and Regulation) Act, 1951.

- The Act was passed by Parliament under the above two heads of the Union and Concurrent Lists.

The SC’s Verdict on Taxing Industrial Alcohol:

- The main question before the court:

- The court's primary concern was whether the term "intoxicating liquor" could also encompass "industrial alcohol."

- States argued that they should regulate industrial alcohol, given its potential misuse in creating illegal consumable alcohol.

- Majority opinion:

- The majority, led by Chief Justice of India (CJI) D Y Chandrachud, along with eight other justices, ruled in favour of the states.

- They reasoned that the term “intoxicating liquor” under Entry 8 of List II (State List) should be interpreted broadly, covering everything from the production of raw materials to consumption.

- The court affirmed that states have the power to tax both alcoholic beverages and industrial alcohol, which can produce intoxication or pose health risks.

- The court disagreed with the Centre’s argument that industrial alcohol falls under its jurisdiction due to its inclusion in the 1951 Act.

- Dissenting opinion:

- Justice B V Nagarathna dissented, arguing that the Centre should retain control over industrial alcohol.

- She maintained that industrial alcohol, by its nature, should not fall under the definition of intoxicating liquor, despite its potential misuse.

- In her view, the Centre's control over industries, as outlined in the 1951 Act, should prevent states from regulating industrial alcohol.

Implications of SC’s Verdict on Taxing Industrial Alcohol:

- Overturned a previous judgement:

- The majority ruling overturned the SC's 1990 judgement in Synthetics & Chemicals Ltd vs State of Uttar Pradesh, which had held that states could not tax industrial alcohol.

- The latest decision affirms that states have the legislative competence to regulate and tax industrial alcohol, even though it is non-potable.

- Impact on States' revenue:

- The court’s decision significantly impacts state revenues, with alcohol taxation already being a major source of income.

- For example, Karnataka raised its Additional Excise Duty (AED) on Indian-made liquor by 20% in 2023.

- The ruling reaffirms states' ability to control this critical revenue stream.

- Federal balance and Centre-State relations:

- The ruling addressed the delicate balance between state and central powers.

- The majority emphasised that, when constitutional entries overlap, the interpretation that preserves federal balance should prevail.

- In this case, giving states the power over industrial alcohol aligns with maintaining that balance, avoiding redundancy in constitutional provisions.

- This decision follows a similar 8:1 majority ruling (in July 2024), which upheld states' authority to levy royalties on mineral extraction and tax the lands where mines are located.