Why in news?

A nine-judge bench in the Supreme Court has ruled by majority that states have legislative competence to levy taxes on minerals and mineral-bearing lands in addition to the royalty imposed by the Centre.

The case, Mineral Area Development Authority v M/s Steel Authority of India, which had been pending for more than a quarter century, was decided by an 8-1 split.

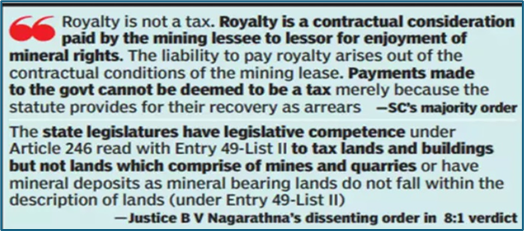

Through the judgment, the court clarified that the royalty charged on mining activities is not a tax; instead, it is considered a form of contractual payment made by miners to the Central government for the extraction of minerals.

This decision reinforces the states' power to generate revenue from mineral resources while maintaining the contractual nature of the royalty payments to the Centre.

What’s in today’s article?

- Background

- Key highlights of the recent judgement

Background

- Mining and Royalties

- Royalties refer to the fees paid to the owner of a product in exchange for the right to use that product.

- E.g., if a movie studio wants to use an existing piece of music by a specific artist in their new film, they will have to pay a royalty fee that goes to the artist.

- The issue of whether royalties on mining activities constitute a tax has been a longstanding legal question in India.

- Under Section 9 of the Mines and Minerals (Development and Regulation) Act, 1957 (MMDRA), entities holding mining leases are required to pay royalties to the owner of the land, which could be a state government.

- This raised the question of whether these royalties are a form of tax when the state is the lessor.

- The Supreme Court first addressed this question in the 1989

- The Supreme Court first addressed this question in the 1989 case India Cement Ltd v State of Tamil Nadu.

- A seven-judge Bench heard a challenge by the company to a Tamil Nadu law imposing a cess on land revenues, including royalties.

- A cess is a form of tax levied by the government on tax with specific purposes till the time the government gets enough money for that purpose.

- The court ruled that while states can collect royalties, they cannot impose taxes on mining activities, as the Central government has overriding authority over the regulation of mines and mineral development under Entry 54 of the Union List.

- In this judgement, the apex court opined that royalty is a tax, and as such a cess on royalty being a tax on royalty, is beyond the competence of the State Legislature.

- The court controversially stated, "royalty is a tax," leading to questions about the interpretation of royalties as a tax.

- 2004 case State of West Bengal v Kesoram Industries Ltd.

- This statement sparked further legal debate and confusion, leading to the 2004 case State of West Bengal v Kesoram Industries Ltd.

- Here, a five-judge Constitution Bench identified a typographical error in the India Cement decision, clarifying that it should have stated "cess on royalty is a tax" rather than "royalty is a tax."

- The court held that royalties themselves are not taxes but could not overrule the India Cement decision due to the smaller size of the bench.

- 2011 Mineral Area Development Authority case

- In 2011, during the Mineral Area Development Authority case, the Supreme Court noted the conflict between the Kesoram Industries and India Cement rulings.

- Recognizing the direct implications for the case at hand, the court referred the matter to a nine-judge bench to conclusively determine whether royalties are a form of tax.

- This led to the recent clarification by the nine-judge bench that royalties are not taxes but contractual payments, thus resolving the long-standing ambiguity.

Key highlights of the recent judgement

- Majority held that a royalty is not a tax

- The majority held that a royalty is not a tax because there is a conceptual difference between royalties and taxes.

- Royalties are based on specific contracts or agreements between the mining leaseholder and the lessor (the person who leases the property) who can even be a private party.

- Also, taxes are meant for public purposes such as welfare schemes and creating public infrastructure.

- On the other hand, the payment of royalties is to a lessor in exchange “for parting with their exclusive privileges in the minerals”.

- States have the power to tax ‘mineral development

- The Supreme Court considered:

- whether states have the authority to tax mineral development activities;

- or if such taxes fall exclusively under the jurisdiction of the Central government under the Mines and Minerals (Development and Regulation) Act, 1957 (MMDRA).

- This issue arises from the provisions in the Seventh Schedule of the Constitution of India.

- The State List grants States the exclusive power to legislate on “taxes on mineral rights subject to any limitations imposed by Parliament by law relating to mineral development” (Entry 50).

- Conversely, Entry 54 of the Union List gives the Central government the power to regulate mines and mineral development.

- It empowers the Parliament by law to be expedient in the public interest.

- According to the earlier India Cement decision, royalties collected by states under the MMDRA were considered a form of tax, precluding states from imposing additional taxes.

- However, the court in the Mineral Area Development Authority case determined that royalties are not taxes.

- This meant that royalties do not fall under “taxes on mineral rights” as per Entry 50 of the State List.

- The court concluded that while the MMDRA provides states with royalties as a revenue stream, it does not restrict states from imposing taxes under Entry 50.

- Furthermore, the court clarified that Parliament’s authority under Entry 54 does not extend to imposing taxes, as that power belongs solely to state legislatures.

- However, Parliament can impose “any limitations,” including prohibitions, on states’ taxing powers under Entry 50.

- The court also recognized that states have the power to tax the land where mines and quarries are located, as this includes:

- all types of lands; and

- covers everything under or over land.

- Such taxes are not affected by the MMDR Act, thereby affirming states’ rights to levy taxes related to mineral development activities.

- Dissent by Justice Nagarathna

- Justice Nagarathna dissented from the majority opinion in the Supreme Court's ruling regarding royalties and the taxation of mineral development activities.

- She argued that royalties under the MMDRA should be considered a tax to promote mineral development in India.

- According to her, the primary goal of the MMDRA is to encourage mineral development and mining activities.

- Allowing states to impose additional levies and cesses on top of the royalties would undermine this objective.

- Justice Nagarathna further opined that the passage of the MMDRA effectively reduced the states' powers to impose taxes on mineral development.

- She stated that the Act grants states the ability to collect royalties, which she views as a form of tax, while providing Parliament and the Central government with comprehensive control over mineral development.