Why in News?

The Central Board of Direct Taxes (CBDT) has notified the National Mission for Clean Ganga (NMCG) as an authority under the Income Tax (IT) Act, 1961.

This grants NMCG income tax exemptions, aiding its functioning under the Namami Gange Programme.

What’s in Today’s Article?

- Namami Gange Programme

- Recent Developments

- Background and Legal Transition of NMCG

- Income Tax Issues Related to NMCG

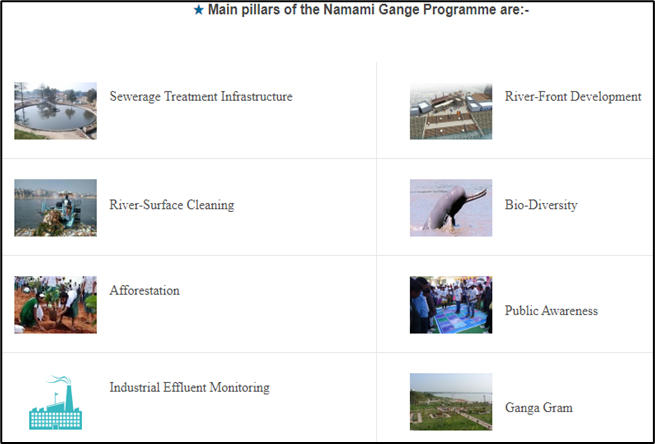

Namami Gange Programme:

- It is an integrated conservation mission, approved as ‘Flagship Programme’ by the Union Government in 2014 with budget outlay of Rs.20,000 Crores.

- It is administered by the Ministry of Jal Shakti's Department of Water Resources, River Development and Ganga Rejuvenation, to accomplish the twin objectives of -

- Effective abatement of pollution,

- Conservation and rejuvenation of National River Ganga.

- The program would be implemented by the National Mission for Clean Ganga (NMCG), and its state counterpart organisations i.e., State Program Management Groups (SPMGs).

- NMCG is the implementation wing of National Ganga Council (NGC), which replaced the National Ganga River Basin Authority.

- NGC was created in 2016 under the River Ganga (Rejuvenation, Protection and Management) Authorities Order, 2016.

- NGC oversees efforts to clean and rejuvenate the Ganga River, and is headed by the PM.

- In order to implement the programme, a three-tier mechanism has been proposed for project monitoring comprising of:

- A high-level task force chaired by Cabinet Secretary assisted by NMCG at the national level,

- State level committee chaired by Chief Secretary assisted by SPMG at the state level, and

- District level committee chaired by the District Magistrate.

- Its implementation has been divided into -

- Entry-Level Activities (for immediate visible impact),

- Medium-Term Activities (to be implemented within 5 years of time frame) and

- Long-Term Activities (to be implemented within 10 years).

Recent Developments:

- Legal basis of the CBDT notification:

- Clause 46A of Section 10, IT Act, 1961: Exemption for income of bodies constituted under a Central/State Act for specified purposes. NMCG was constituted under the Environment (Protection) Act, 1986.

- Effective from: Assessment Year (AY) 2024-25.

- Condition: NMCG must continue as an authority under the Environment (Protection) Act with relevant purposes.

- Significance: It ensures financial autonomy and operational efficiency for NMCG, crucial for the effective execution of the Namami Gange Programme.

Background and Legal Transition of NMCG:

- Initial status: Registered as a society (August 12, 2011) under the Societies Registration Act, 1860.

- Upgradation: Declared an ‘authority’ (October 7, 2016) under the Environment (Protection) Act, 1986.

- Technical issue: Despite this transition, PAN status continued as Association of Persons (AOP), attracting scrutiny and tax demands.

Income Tax Issues Related to NMCG:

- Tax demands: NMCG faced income tax demands totaling ₹243.74 crore.

- Condonation by CBDT:

- Allowed delayed filing of revised returns for the three assessment years.

- Enables NMCG to claim tax exemptions retrospectively.

- Reason for relief: Jal Shakti Ministry intervened with the Ministry of Finance.