Why in News?

The fall in household savings has been at the heart of recent debates in India, which is brought about by a drastic reduction in net financial savings.

What’s in Today’s Article?

- Interpreting Lower Financial Savings

- Implication of Higher Debt Burden

- What are the Macroeconomic Implications of Fall in Household Savings?

Interpreting Lower Financial Savings:

- Meaning:

- The net financial savings of the household is the difference between its gross financial savings and borrowing.

- The gross financial savings of a household is the extent to which its financial assets change during a period.

- The financial assets of households typically comprise bank deposits, currency and financial investments in mutual funds, pension funds, etc.

- Though household borrowing includes credit from non-bank financial corporations and housing corporations, the bulk of the borrowing comprises credit from commercial banks.

- Three factors that can potentially bring about a reduction in household net financial savings:

- Households typically finance their additional consumption expenditure by increasing their borrowing or depleting their gross financial savings.

- When households finance higher tangible (physical) investment by increasing their borrowing or depleting their gross financial savings.

- When interest payment of a household increases, say due to higher interest rates.

- Analysing the Above 3 Factors:

- The first factor hardly played any role in the sharp reduction in gross financial savings in 2022-23 as the consumption to GDP ratio remained largely unchanged between 2021-22 (60.95%) and 2022-23 (60.93%).

- The second factor played only a limited role. While the gross financial savings to GDP ratio declined from 7.3% to 5.3% in 2022-23, household physical investment to GDP ratio increased only from 12.6% to 12.9%.

- Though higher borrowing is partly financed by interest income from financial assets, it can be largely attributed to higher interest payments of the household in the recent period.

Implication of Higher Debt Burden:

- The rise in household debt burden has two concerns for the macroeconomy - (debt repayment and financial fragility) and (the implication on consumption demand).

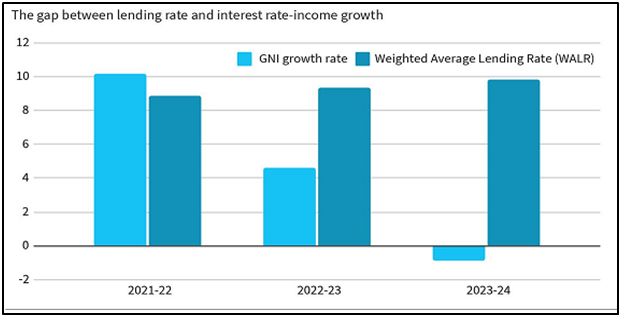

- Since the repayment capacity depends on the income flow, a key criterion for evaluating a household’s debt sustainability is the difference between interest rate and the income growth rate.

- On the flip side, the interest payments from the households are the interest income of the financial sector.

- If households fail to meet their debt repayment commitments, then it reduces the income of the financial sector and deteriorates their balance sheets.

- This in turn can have a cascading effect on the macroeconomy if the latter responds by reducing their credit disbursement to the non-financial sector.

- Over and above disposable income, the consumption expenditure of the household can be affected by their wealth, debt, and interest rate.

- Reduction in household wealth can lead to lower consumption expenditure as households may attempt to preserve their wealth position by increasing their savings.

What are the Macroeconomic Implications of Fall in Household Savings?

- The households are susceptible since both the stock indicator of debt to net worth and the flow indication of liabilities to disposable income show an increasing tendency.

- Higher interest rates, which are used as a policy tool to combat inflation by lowering macroeconomic output and employment, can cause households' debt levels to rise and even put them in danger of debt trap.

- The implications of high interest rate on debt burden can have an adverse impact on the consumption of the households and consequently for aggregate demand.

- The household balance sheet trends indicate a broader change in the structure of the economy.

- A certain amount of financialisation of the economy is indicated by the shift in the asset side of the household balance sheet from production-based to monetary or financial exchange-based.

- This will make the five trillion-dollar economy both fragile and jobless.