Context

- The Old Pension Scheme (OPS) has been recently figured as a prominent poll promise in the Himachal Pradesh and Gujarat Assembly elections.

- Earlier, the states of Rajasthan, Chhattisgarh and Jharkhand have reverted to the non-contributory defined benefit OPS from April 2022 from reform-oriented contributory National Pension System (NPS).

- The article while highlighting the underlying differences in OPS and NPS presents a broad vision about pensions system in India.

National Pension Scheme (NPS):

- NPS is a voluntary and long-term investment plan for retirement under the purview of the Pension Fund Regulatory and Development Authority (PFRDA), Ministry of Finance, Government of India.

- It was launched in January 2004 for government employees when the Government of India decided to stop defined benefit pensions for all its employees who joined after 1 April 2004.

- It was opened up for all citizens of India between the age of 18 and 70 and for Overseas Citizen of India (OCI) card holders and Persons of Indian Origin (PIO).

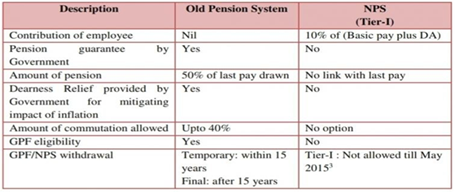

Old Pension Scheme

- The old pension scheme (discontinued in 2004) assures life-long income, post-retirement.

- Usually, the assured amount is equivalent to 50% of the last drawn salary. The Government bears the expenditure incurred on the pension.

Why there is demand to restore OPS?

- Rising pension bill:

- For instance, the pension expenditure has increased from ~16 to 18% in the last five years as a percentage of revenue expenditure.

- According to the CAG, the combined pension bill of 30 states and UTs in 2019-20, was ~62% (Rs 3.38 lakh crore) of their combined expenditure (Rs 5.47 lakh crore) on salary and wages.

- The latest edition of the Handbook of Statistics on Indian states, released by RBI revealed that the combined pension expenditure of all states and UTs has doubled to Rs 3.45 lakh crore in 2019-20 from Rs 1.63 lakh crore in 2013-14.

- Lesser revenue for development expenditure:

- For instance, during 2020-21, only about one-third of the state’s total revenue receipts were available for developmental outlay.

- The Own Tax Revenues (OTR) of states which comprises taxes like State GST, State Excise, Stamp Duty and Registration Fees, Land Revenue, etc., has also remained very low in recent years, thus putting more strain on exchequer by NPS contribution.

- Trade unions have opposed the NPS because it does not offer assured returns, no withdrawals till retirement at 60, corpus is not tax free on maturity.

India’s pension system: Global comparison

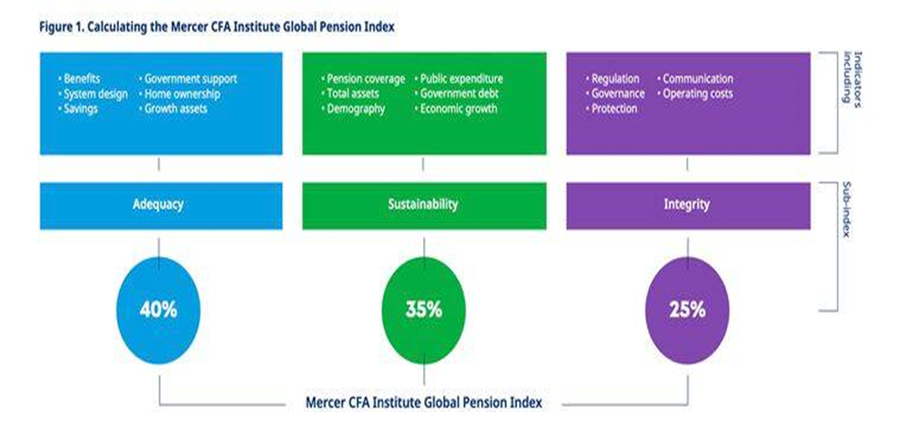

- The Mercer CFA Institute Global Pension Index ranks the pension systems across the world.

- The 2022 edition of this index ranks India’s pension system at 41 (Grade D) out of the 44 countries it considers. The index was topped by Iceland, Netherlands and Denmark (Grade A).

- This trend is concerning since India has consistently ranked low on this index even when only 16 countries were analysed in 2011.

Limitation of India’s pension system

- Alarming exclusions: At least 85% current workers are not members of any pension scheme, and in their old age likely to remain uncovered or draw only social pension.

- Of all elderly, 57% receive no income support from public expenditure, and 26% collect social pension as part of poverty alleviation.

- Few cornering major chunk: 11.4% of the elderly draw defined benefit as government ex-workers (or their survivors), cornering 62% of system expense.

- Pension burden on state governments: The system for old age income support entailed 11.5% of public expenditure, and state governments bear more than 60%.

- Rising interest payments: Contributory program funds invested in government securities soak up 40% of all interest payment of state governments.

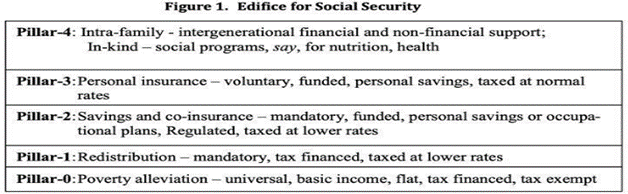

Pension framework by World Bank

- Zero pillar: A non-contributory basic pension from public finances to deal explicitly with the poverty-alleviation objective.

- First pillar: A mandated public pension plan with contributions linked to earnings, with the objective of replacing some pre-retirement income.

- Second pillar: Mandated defined contribution (DC) with individual accounts in occupational or personal pension plans with financial assets.

- Third pillar: Voluntary and fully funded occupational or personal pension plans with financial assets that can provide some flexibility when compared to mandatory schemes.

- Fourth pillar: A voluntary system outside the pension system with access to a range of financial and non-financial assets and informal support such as family, healthcare and housing.

Way ahead

- The retirement benefits as state obligation have origins in erstwhile monarchies, where meritorious public servants were rewarded benefits upon retirement.

- However, the modern states are longer-lived than monarchies and may extend benefits beyond the life of the public servant.

- The working paper by National Institute of Public Finance and Policy (NIPFP) hence calls for adequate calibration, as it could cause a sharp escalation in resultant benefits otherwise.

- It has also tweaked the World Bank framework for India as mentioned in the table below:

Conclusion

- Pension reforms are fundamentally important for the nation’s financial health and merely fluctuating between OPS and NPS is not right as the earlier is problematic on the count of sustainability while later suffers from inter-generational inadequacy. Thus, India needs afresh debate to relook its pension system.