In News:

- Recently, the Minister of Cooperation, Government of India, stated that cooperative banks will not be treated as "second class," but that they must adopt modern and transparent banking methods in order to compete.

- The Minister urged the Urban Cooperative Banks (UCBs) to implement institutional reforms, as they account for only 3.25% of total bank deposits and 2.69% of total advances in the country.

What’s in today’s article:

- Cooperative Banking in India (About, brief history, governed by, structure, objectives, features, advantages, challenges)

- News Summary

Cooperative Banking in India:

- About Co-operative banks:

- A co-operative bank is a financial entity which belongs to its members, who are both the owners and customers of their bank.

- It is often established by people belonging to the same local or professional community having a common interest.

- It is formed to promote the upliftment of financially weaker sections of the society and to protect them from the clutches of money lenders.

- Brief history:

- The problem of rural credit was the key reason behind the advent of the co-operative movement in India.

- The movement began with the passage of the Co-operative Societies Act in 1904.

- The next addition was the Co-operative Societies Act, 1912, focussed on the need for regulation of such societies.

- This led to the establishment of appropriate bodies to oversee their functioning.

- Who governs these banks?

- In India, co-operative banks are registered under the States Cooperative Societies

- They also come under the regulatory ambit of the Reserve Bank of India (RBI) under two laws:

- the Banking Regulations Act, 1949, and

- the Banking Laws (Co-operative Societies) Act, 1955.

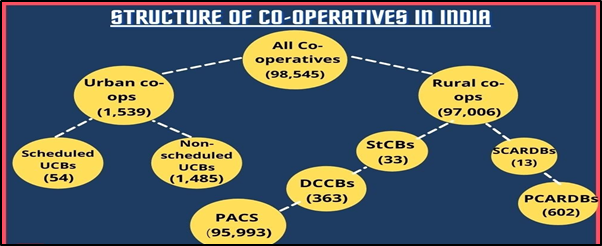

- Structure:

- Broadly, co-operative banks in India are divided into two categories - urban and rural.

- Rural cooperative credit institutions could either be -

- Short-term (State Co-operative Banks, District Central Co-operative Banks, Primary Agricultural Credit Societies) or

- Long-term (State Cooperative Agriculture and Rural Development Banks (SCARDBs) or Primary Cooperative Agriculture and Rural Development Banks (PCARDBs)) in nature.

- On the other hand, Urban Co-operative Banks (UCBs) are either scheduled or non-scheduled.

- Scheduled and non-scheduled UCBs are again of two kinds - multi-state and those operating in single state.

- Objectives of Cooperative banks:

- To provide rural financing and micro-financing.

- To remove the dominance of money lenders and middlemen.

- To provide credit services to agriculturalists and weaker sections of the society at comparatively lower rates.

- To provide financial support and personal financial services to small scale industries, housing financial assistance, etc.

- Features:

- Their co-operative structure is designed on the principles of cooperation, mutual help, democratic decision making and open membership.

- It follows the principle of ‘one shareholder, one vote’ and ‘no profit, no loss.

- Cooperative banks differ from commercial banks on the grounds of organisation, governance, interest rates, the scope of functioning, objectives and values.

- Advantages:

- Easy to form:

- Registration and legal requirements are comparatively easy compared to traditional banks.

- It takes a group of 10 adults to form a cooperative bank and needs a base capital of 25 lakhs only as compared to 100 crores of Small Finance Banks.

- Alternative credit source: They act as an effective alternative to traditional money lending systems.

- Cheap credit: They provide a high-interest rate to members for their investments and low lending interest rate.

- Encouragement of savings and investments: They have encouraged the habit of thrift among the masses (masses tend to invest and save their money).

- Advancement in farming: Cooperative societies provide credit to agriculturalists at cheaper rates to buy inputs, warehousing facilities, marketing assistance, etc.

- Challenges:

- Small capital base: Cooperative banks can begin with a capital base of 25 lakhs, making it difficult to account for a portion of that capital as working capital and raising working capital.

- Political interference: Politicians use them to boost their vote bank and usually get their representatives elected to the board of directors in order to gain unfair advantages (such as loan approval that is later written off).

- RBI oversight is weak: The supervision of RBI is not as stringent on cooperative banks as compared to commercial banks. RBI inspects the books of these banks only once a year.

- As a result, the Punjab and Maharashtra Cooperative Banks (PMC Bank) have recently virtually collapsed.

- The PMC Bank had violated RBI norms by lending heavily (73% of its assets) to one client-real-estate firm (HDIL), which itself is facing bankruptcy proceedings.

- Dual control: Cooperative banks are controlled by RBI and by their respective State government which poses a problem in coordination and management.

- Poor professional management and technological advancement: Cooperative banks are often reluctant to adopt new technologies (like computerised data management) and professional management in the banks is often missing due to lack of training of personnel because of lack of funds.

- Dependence of finance: They depend heavily on RBI, NABARD and the government for refinancing facilities. It depends on the government for capital rather than on its members.

- Overdue loans: Overdue loans of cooperative banks are increasing yearly, restricting the recycling of funds which in turn affects the lending and borrowing capacity of the bank.

News Summary:

- Speaking at the National Conclave on Scheduled and Multi-State Urban Cooperative Banks and Credit Societies (NAFCUB), the Minister of Cooperation said that Urban Cooperative Banks (UCBs) will be treated equally.

- They will not get any special favour but will not be treated like a second-grade citizen in respect of be it taxation, the Banking Regulation Act, 1949 or the RBI’s norms.

- The responsibility of development lies with the cooperative sector and the UCBs.

- For this, they should undertake institutional reforms like transparency in recruitment and implementation of a robust accounting system.

- There is a need to bring in new people, young people and professionals in managerial roles, who will take cooperative forward.

- By matching human resources of the private sector banks and nationalised banks, a sense of competition will be promoted.