Objective:

- The bill seeks to provide for a comprehensive mechanism to ban the unregulated deposit schemes other than deposits taken in the ordinary course of businesses and to protect the interest of depositors.

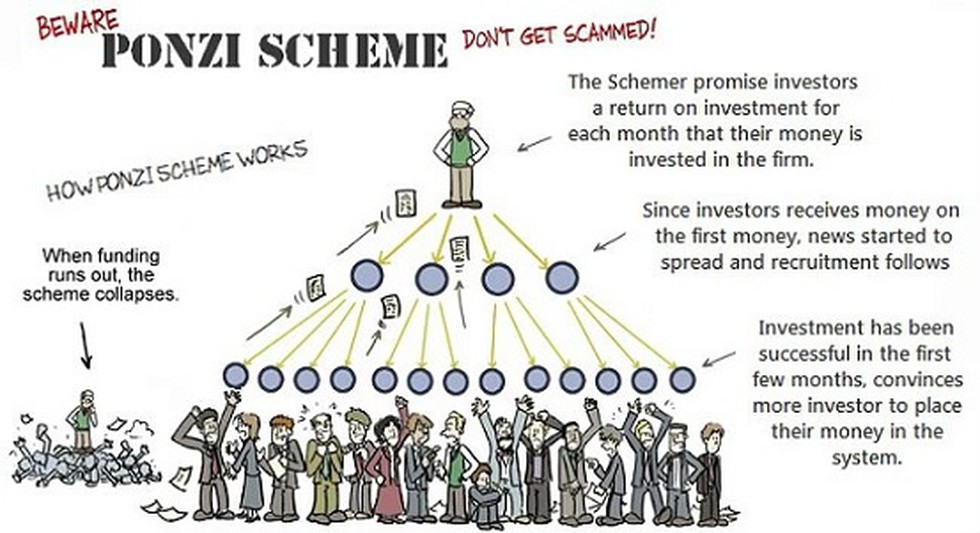

- The bill after becoming an act will work as a crackdown on Ponzi schemes. the bill will help protect the interests of poor people and their hard-earned money.

Salient features of the Bill:

- Unregulated deposit scheme: The Bill bans unregulated deposit schemes. A deposit-taking scheme is defined as unregulated if it is taken for a business purpose and is not registered with the regulators listed in the Bill.

- Deposit taker: The Bill defines deposit takers as an individual, a group of individuals, or a company who asks for (solicits), or receives deposits. Banks and entities incorporated under any other law are not included as deposit takers.

- Competent Authority: The Bill provides for the appointment of government officers, not below the rank of Secretary to the state or central government, as the Competent Authority. The Competent Authority will have powers similar to those vested in a civil court. The Competent Authority may:

- provisionally attach the property of the deposit taker, as well as all deposits received,

- summon and examine any person it considers necessary for the purpose of obtaining evidence, and

- order the production of records and evidence.

- Designated Courts: The Bill provides for the constitution of one or more Designated Courts in specified areas. The Court will seek to complete the process within 180 days of being approached by the Competent Authority.

- Central database: The Bill provides for the central government to designate an authority to create an online central database for information on deposit takers. All deposit takers will be required to inform the database authority about their business.

- Offences and penalties: The Bill defines three types of offences, and penalties related to them. These offences are:

- running (advertising, promoting, operating or accepting money for) unregulated deposit schemes,

- fraudulently defaulting on regulated deposit schemes, and

- wrongfully inducing depositors to invest in unregulated deposit schemes by willingly falsifying facts.