About:

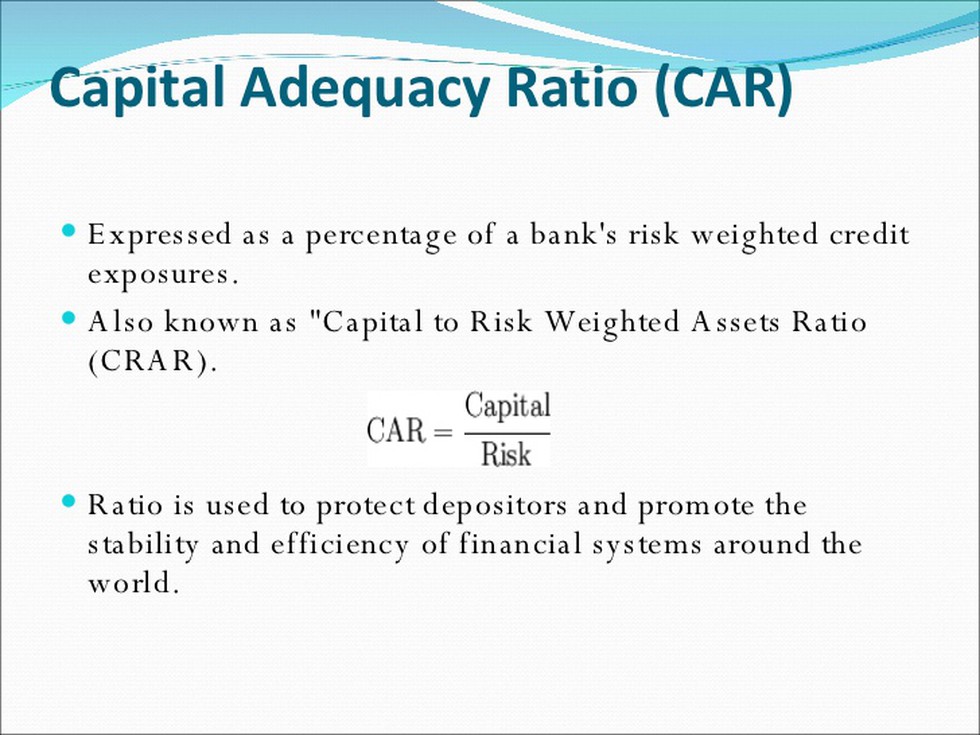

- Capital Adequacy Ratio (CAR) is the ratio of a bank’s capital in relation to its risk weighted assets and current liabilities. It is measured as:

- Capital Adequacy Ratio = (Tier I + Tier II + Tier III (Capital funds)) /Risk weighted assets

- The risk weighted assets take into account credit risk, market risk and operational risk.

- It is decided by central banks and bank regulators to prevent commercial banks from taking excess leverage and becoming insolvent in the process.

- Criteria:

- The Basel III norms stipulated a capital to risk weighted assets of 8%.

- However, as per RBI norms, Indian scheduled commercial banks are required to maintain a CAR of 9% while Indian public sector banks are emphasized to maintain a CAR of 12%.

Need of High CAR: Recent Debate

- Government is complaining about the ‘unnecessary’ high capital requirements. Govt. wants the capital adequacy ratio of banks to be at 8% as per Basel norms, but RBI has prescribed 9%.

- Arguments by of RBI:

- Maintaining adequate levels of bank capital enable banks to sustain unexpected losses without defaulting on its obligations, especially deposits.

- Though higher capital involves costs, “there is no free lunch”. Also, the costs to the economy are offset by the savings made in the preventing Banking crises.

- It is a misconception that capital was some sort of “rainy-day fund” and that the economy was deprived of that money. Instead, the capital maintained by banks is deployed on its balance sheet towards creating assets.

- While the argument that higher capital requirement leads to lower credit growth is ‘mathematically correct’ but data shows that credit growth in the Indian economy is in line with nominal GDP growth.

- RBI also warned that in the past, high levels of credit growth due to ‘supply push’ have resulted in NPAs in the banking system.

- Any loosening of the prudential norms may result in a reset of their credibility in the international markets. This might push the clients to other banks which are compliant with Basel standards.