Why in news?

White Papers recently released by Kerala and Tamil Nadu — two of India's most socially and economically advanced States — described their outstanding debt as alarming.

This has revived a debate about State finances. State debt is often unfairly dismissed as fiscal mismanagement, when it may instead reflect a mismatch between development aspirations and the limited fiscal capacity of States.

What’s in Today’s Article?

- The Core Fiscal Dilemma

- How States Fund Themselves — and Fall Short?

- Kerala's Spending: Locked Into Day-to-Day Costs

- The Investment Trap

- The China Comparison: A Different Model

- Rethinking State Debt

The Core Fiscal Dilemma

- The heart of the problem lies in a structural imbalance in Indian federalism. Debt builds up over years through deficits — when a government's spending exceeds its tax and other receipts.

- The key mismatch is this: the power to raise taxes rests largely with the Union government, but a larger share of overall public spending is borne by the States.

- Most State expenditure goes to areas that directly touch people's lives:

- Social sectors — health and education

- Economic sectors — agriculture and irrigation

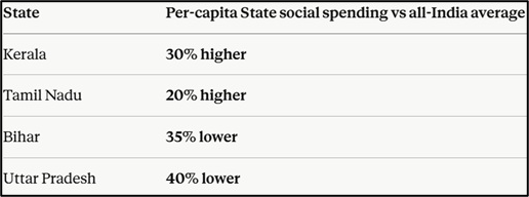

- In Kerala, high social-sector spending since the 1960s has been central to its social progress. Comparative per-capita social expenditure (2020–23) shows the divide clearly:

How States Fund Themselves — and Fall Short

- States meet expenditure through two main channels:

- Own revenues — mainly State GST (SGST) and sales tax.

- Union transfers — devolution, grants, and loans.

- Kerala's case illustrates the squeeze. It has a good record of raising own-tax revenue — 1.5 times the all-India per-capita average.

- Yet its share in Union tax devolution was just 1.92%, lower than its 2.6% share of India's population in 2023–24.

- In effect, a State that taxes itself well still receives proportionally less from the centre. The gap between expenditure and receipts is bridged through market borrowings, on which States pay interest.

Kerala's Spending: Locked Into Day-to-Day Costs

- A closer look at Kerala's budget reveals why fiscal space is so tight. Of its limited resources, only about 10% goes to capital expenditure (which builds future productive capacity).

- The rest is revenue (day-to-day) expenditure:

- ~20% on salaries (mainly teachers, nurses, doctors, police)

- 15.3% on pensions

- 16.5% on interest on market borrowings

- With such a large share pre-committed to salaries, pensions, and interest, very little is left to invest in the future.

The Investment Trap

- This traps Kerala in a genuine dilemma:

- If it cuts revenue expenditure (pensions, employees) to free up money, it risks eroding its hard-won social-sector strengths.

- But it urgently needs large investments in infrastructure, higher education and research, and public transport to compete in modern, knowledge-intensive sectors.

- The human cost is visible: educated young people are leaving Kerala in large numbers because the State cannot create opportunities matching their aspirations.

- There is also a striking paradox — the government's weak fiscal capacity contrasts with visible private affluence (large houses, expensive cars, dense gold shops), threatening to widen inequality.

The China Comparison: A Different Model

- Analysts contrast India's constraints with China's model of decentralised investment-led growth:

- In China, provinces and local governments undertake the bulk of growth-boosting investment, borrowing heavily against the country's large domestic savings pool.

- Their efforts are coordinated through central government planning.

- They raise resources via local government bonds (LGBs), land sales, and off-budget borrowing through local government financing vehicles (LGFVs), on top of central transfers.

- The cost difference is stark. Chinese local governments borrow from their banking system at roughly 2%, whereas Indian States pay far more.

- State Development Loans (SDLs) — the securities States issue to borrow from the market — carry interest of about 6.5% to 7.5%.

- This is 0.25 to 0.75 percentage points higher than the rate at which the Union government itself borrows, and significantly more expensive than the cost Chinese local governments face.

- In other words, Indian States are squeezed twice over: they face both limits on how much they can borrow and a markedly higher cost of debt, which further tightens the noose around their finances.

Rethinking State Debt

- In India, government bonds are mostly bought by domestic institutions like banks and insurance companies. These institutions use the savings that ordinary people deposit with them. So when the government borrows, it is really borrowing from its own citizens.

- Hence, a government that borrows to expand welfare and create opportunities is doing something far more useful than one that refuses to spend at all.

- Against this backdrop, India needs a system that allows State governments to use the country's own savings more easily and at a lower cost, so they can fund well-planned development projects.